In today’s rapidly evolving financial landscape, understanding how money works is more crucial than ever. Whether you’re a young adult starting your career, an early-career professional, or someone looking to improve your financial health, developing financial literacy is your most important step toward achieving financial independence.

The year 2026 brings new opportunities and challenges: digital banking, cryptocurrencies, AI-driven financial tools, inflation concerns, and changing retirement systems. These shifts make it essential to equip yourself with the right knowledge and skills.

This guide aims to demystify personal finance, providing you with practical, easy-to-understand strategies on budgeting, saving, investing, managing debt, and protecting your assets. With a clear roadmap, you’ll learn how to make informed decisions that serve your personal goals and secure your financial future.

What Is Financial Literacy?

Financial literacy is the ability to understand and effectively use various financial skills such as budgeting, saving, investing, and managing debt to make sound financial decisions. It involves knowledge of basic financial concepts, familiarity with financial products, and the capacity to plan for future needs.

Why is it so important? Because money management is a vital life skill. Without a solid understanding, individuals risk falling into debt, missing investment opportunities, or being vulnerable to financial scams.

Why Financial Literacy is important in 2026?

The digital age has transformed how we access and manage money. Mobile banking apps, digital wallets, cryptocurrencies, and AI financial advisors are now common. While these innovations offer convenience, they also require a basic understanding to harness their benefits fully and avoid pitfalls.

Furthermore, global economic shifts like inflation, interest rate changes, and geopolitical tensions meaningfully impact personal finances. Being financially literate allows you to adapt strategies accordingly.

read more about Medtronic: Company Overview, Revenue Model and Growth Strategy

Core Components of Financial Literacy

Money Management: Budgeting, expense tracking, and cash flow control

Saving & Emergency Funds: Building reserves for unexpected expenses

Investing & Wealth Building: Growing assets through stocks, bonds, ETFs, real estate

Debt & Credit Management: Using credit wisely and avoiding debt traps

Risk Management & Insurance: Protecting assets and income

Retirement Planning: Preparing financially for life after work

Why Financial Literacy Matters in 2026

The importance of financial literacy continues to grow in 2026 for several reasons:

1. Digital Banking and Fintech Innovations

The proliferation of mobile banking platforms, digital wallets, and fintech apps simplifies transactions but introduces new risks: cyber threats, scams, and privacy concerns. Understanding how to secure accounts, recognize fraud, and use these tools effectively is vital.

2. Cryptocurrency and Blockchain Technology

Cryptocurrencies like Bitcoin and Ethereum are mainstream investment options. While they can diversify your portfolio, they are highly volatile and complex. Basic literacy helps you navigate these markets safely.

3. Inflation and Economic Volatility

Inflation erodes money’s purchasing power. Currently, global inflation remains a concern due to supply chain issues and monetary policies. Knowledge of how inflation impacts savings and investments enables better decision-making.

4. Evolving Retirement and Pension Systems

Retirement plans are shifting worldwide. Defined-benefit plans are decreasing, replaced by defined-contribution schemes like 401(k)s and IRAs in the US, or SIPPs and ISAs in the UK. Early understanding helps you plan effectively.

5. Global Financial Education Gaps

Despite technological progress, many individuals worldwide lack basic financial knowledge, increasing vulnerability to scams and poor decisions. Education initiatives aim to bridge this gap, emphasizing proactive learning.

6. AI and Automation in Financial Planning

AI-driven tools for budgeting and investment management are becoming accessible. To maximize their benefits, you need to understand how they work, their limitations, and how to interpret their advice.

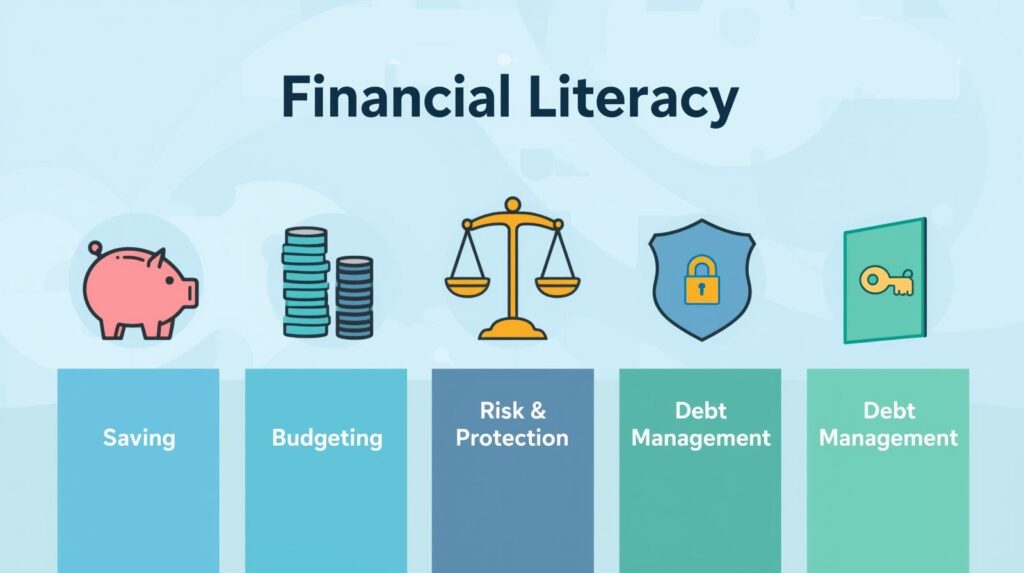

The 5 Pillars of Financial Literacy

Building a solid financial foundation involves mastering these five key areas:

1. Budgeting

This is the cornerstone of financial success. Creating a budget helps you control spending, avoid debt, and save for future goals.

2. Saving

Building a savings buffer provides security and funds for your goals—whether for emergencies, a new car, or a house.

3. Investing

Investing allows your money to grow faster than inflation, helping you build wealth over time.

4. Debt Management

Using credit wisely and paying off debts efficiently prevent financial strain and improve your credit profile.

5. Risk & Protection

Insurance and emergency funds safeguard against unforeseen events that could derail your financial plans.

Budgeting: The Foundation of Financial Success

How to Create a Budget: A Step-by-Step Guide

Step 1: Calculate Your Income

Include all sources: salary, side gigs, rental income, dividends, etc.

Example: Jane earns $4,000 monthly from her job, with an additional $200 from freelance work, totaling $4,200.

Step 2: List Fixed Expenses

These are recurring costs like rent, utilities, insurance, subscriptions.

Example: Rent $1,200, utilities $200, insurance $150, totaling $1,550.

Step 3: Track Variable Expenses

Groceries, dining out, transportation, entertainment.

Example: Groceries $600, dining $300, transportation $150.

Step 4: Set Savings Goals

Decide on monthly savings, e.g., $500 for an emergency fund or future investments.

Step 5: Allocate Funds

Ensure total expenses and savings do not exceed income.

Example: Expenses: $1,550 + $1,050 (variable) + $500 savings = $3,100, leaving $1,100 for discretionary spending.

Step 6: Adjust and Automate

Use apps like Mint, YNAB, or bank tools to track and automate transfers, ensuring consistency.

Budgeting Tools & Apps

Spreadsheets: Flexible and customizable.

Apps: Mint, YNAB, PocketGuard offer automation and alerts.

Envelope Method: Cash-based discipline for spending categories.

Building an Emergency Fund

An emergency fund provides financial security during unforeseen events.

Why It’s Critical

Unexpected expenses, medical emergencies, job loss, urgent repairs can be financially destabilizing. An emergency fund acts as a buffer, reducing reliance on credit or loans.

How Much to Save

Aim for 3–6 months of living expenses. For example, if your monthly expenses are $2,000, target $6,000–$12,000.

Strategies to Build

Set Monthly Savings Targets: Automate deposits into a separate account.

Prioritize: Focus on building the fund before investing heavily.

Use High-Yield Savings Accounts: FDIC-insured in the US, FSCS in the UK.

Real-Life Example

Emma saves $300 monthly in a high-yield savings account. At this rate, she’ll reach her $6,000 goal in 20 months.

Understanding Credit Scores and Reports

The US System

FICO Score Range: 300–850.

Factors: Payment history (35%), amounts owed (30%), length of credit history (15%), new credit (10%), credit mix (10%).

Impact: Determines loan eligibility, interest rates, and insurance premiums.

The UK System

Credit Reports: Managed by agencies like Experian, Equifax.

Factors: Payment history, utilization, account age.

Tips to Improve Your Credit Score

Pay bills on time.

Keep balances below 30% of credit limits.

Avoid opening multiple new accounts simultaneously.

Regularly review your report for errors.

Managing Debt Wisely

Strategies

Prioritize paying off high-interest debts first (debt avalanche).

Use the debt snowball method: pay off smallest debts first for motivation.

Consolidate debts when possible to lower interest rates.

Avoid taking on unnecessary new debt.

Example

Lisa has $3,000 in credit card debt at 18%. She pays $150/month, focusing on high-interest debts first, reducing the total interest paid and clearing debt faster.

Saving vs Investing: What Beginners Must Know

Aspect

Saving

Investing

Purpose

Short-term needs, emergency fund

Long-term wealth growth

Risk

Low

Variable, generally higher

Liquidity

High (cash, savings account)

Varies (stocks, bonds, ETFs)

Returns

Low, interest, inflation-adjusted

Potentially high, dividends, capital gains

Key Takeaway: Save for safety and liquidity; invest for wealth building and retirement.

Investing for Beginners

Stocks

Ownership units in companies.

Example: Buying 10 shares of Apple at $150/share costs $1,500. Over time, as Apple grows, share value and dividends can increase.

Bonds

Loans to governments or corporations.

Example: US Treasury bonds pay fixed interest, considered safer but with lower returns.

ETFs and Index Funds

Diversified baskets tracking indices like the S&P 500.

Example: Investing in an ETF that tracks the S&P 500 provides exposure to 500 large US companies and reduces risk.

Retirement Accounts

US: 401(k), Roth IRA

UK: ISA, SIPP (Self-Invested Personal Pension)

The Power of Compound Interest

Long-term investments benefit from compounding.

Formula:

(A = P × (1 + r)^n)

Where:

A: Future value

P: Principal amount

r: Annual interest rate (decimal)

n: Number of years

Example:

$1,000 invested at 7% annually for 30 years grows to approximately $7,612, illustrating the benefit of starting early.

Inflation and Its Impact

Inflation reduces the purchasing power of money over time, making it harder to buy the same goods and services later. In 2026, inflation remains a concern due to supply chain disruptions, monetary policies, and geopolitical tensions.

How to Protect Against Inflation

Invest in assets that tend to outpace inflation, such as stocks, real estate, or commodities.

Use inflation-linked bonds like TIPS (Treasury Inflation-Protected Securities) in the US or index-linked gilts in the UK.

Financial Literacy in the Digital Age

Online Banking & Fintech Tools

Digital platforms make managing money easier but require understanding security practices. Use strong passwords, enable two-factor authentication, and be cautious of phishing attempts.

Digital Wallets & Contactless Payments

Services like Apple Pay or Google Pay simplify transactions but involve sharing sensitive data; awareness and security are vital.

Cryptocurrency & Blockchain

While digital currencies offer diversification, they are highly volatile and speculative. Educate yourself before investing or using crypto.

AI & Robo-Advisors

Automated investment platforms use algorithms to manage portfolios based on your risk tolerance, making investing accessible but requiring understanding of their strategies.

Common Mistakes Beginners Make

Not tracking expenses, leading to overspending.

Failing to save early, missing the benefits of compounding.

Ignoring credit scores, which influence loan terms.

Overusing credit cards, leading to debt.

Underestimating inflation’s impact.

Investing without research or understanding.

Setting Financial Goals

Clear, actionable goals help you stay motivated and organized. Use the SMART framework:

Specific: Define exactly what you want.

Measurable: Quantify progress.

Achievable: Set realistic targets.

Relevant: Align goals with your values.

Time-bound: Attach deadlines.

Example: “Save $10,000 for a car down payment in 12 months.”

Break goals into short-term (monthly savings), medium-term, and long-term (retirement). Regularly review and adjust as circumstances change.

12-Month Financial Literacy Action Plan

Month

Focus Area

Key Actions

1–2

Assess current financial situation

Track income, expenses, debts

3–4

Create and refine budget

Use apps, automate savings

5–6

Build emergency fund

Save monthly, prioritize safety

7–8

Improve credit score

Check report, pay bills on time

9–10

Learn about investments

Research stocks, ETFs

11–12

Set future goals

Retirement, big purchases

This plan provides a structured approach to building financial skills, ensuring steady progress.

Frequently Asked Questions (FAQs)

Q1: How much should I save each month?

A: Aim to save at least 20% of your net income, adjusting based on your goals and expenses.

Q2: What’s the best way to start investing?

A: Begin with low-cost, diversified ETFs or index funds, invest regularly, and avoid trying to time the market.

Q3: How can I improve my credit score?

A: Pay bills on time, keep balances low, avoid opening many new accounts simultaneously, and review your credit report for errors.

Q4: What’s the difference between stocks and bonds?

A: Stocks represent ownership in a company, offering higher risk and potential returns. Bonds are loans to entities, providing fixed income with lower risk.

Q5: How does inflation affect my savings?

A: Inflation erodes the purchasing power of your cash over time. Investing in assets that outpace inflation helps preserve value.

Conclusion:

Financial literacy is a vital life skill. In 2026, with a foundation of knowledge and disciplined habits, you can navigate complex financial environments confidently.

Begin today, educate yourself, set clear goals, and develop healthy money habits. Your future self will thank you.